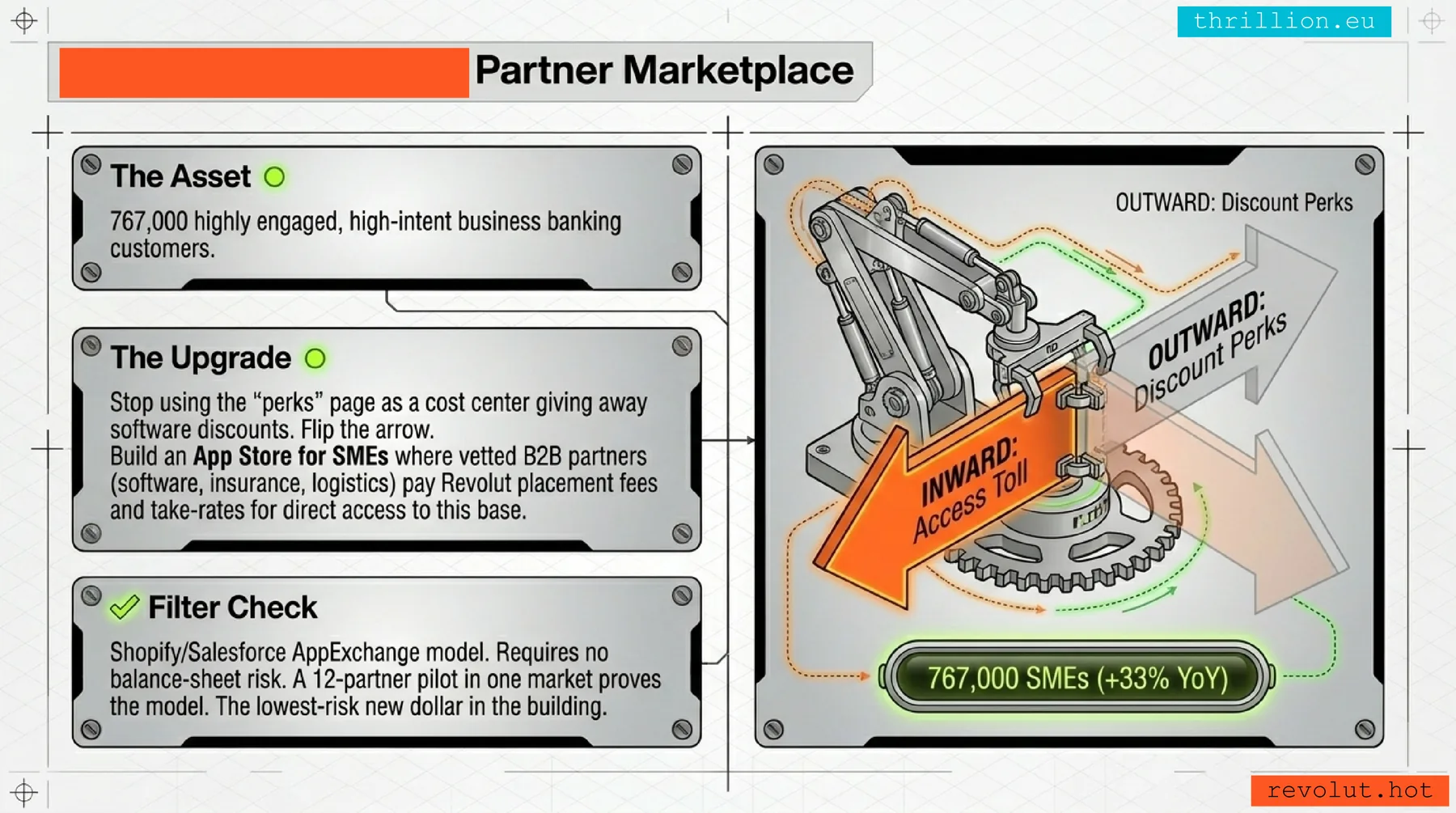

Partial

Claim: merchant network as distribution

SumUp confirms the direction, not the exact product.

The book’s Partner Marketplace thesis was about routing partners through verified businesses. SumUp’s move routes consumers through merchants. Same asset logic; different first wedge.

Confirmed

Claim: accounting is the sticky layer

SumUp × Sage makes the back office explicit.

The MTD product turns payments, invoices, expenses and banking data already inside SumUp into tax-compliance workflow. This supports the ANNA-style thesis without proving ANNA must be acquired.

Diverged

Claim: consolidation route

So far, partnership and organic build beat M&A.

The anti-Revolut idea may still require size. But the first strong data point is SumUp assembling the stack through product and partnership, not a visible merger.

Open

Claim: merchant AI edge node

The AI mini-PC idea gets a better home.

Consumer DePIN hardware remains weak. But a merchant-owned AI appliance next to POS, loyalty, accounting and cashback is now a more plausible SumUp wedge.